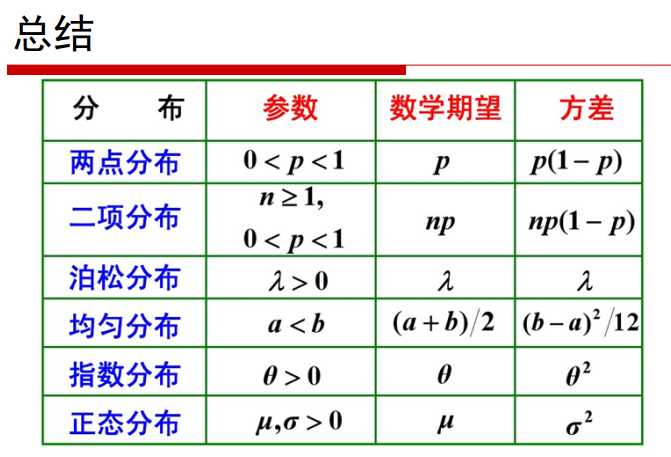

1.两点分布——离散型概率分布

概念:一次试验,若成功随机变量取值为1,成功概率为p; 若失败随机变量取0,失败概率为1-p

期望\(E(X)=1*p+0*(1-p)=p\)

方差

\[

\begin{aligned}

D(X)&=p*(1-p)^2+(1-p)*(0-p)^2\&=p(1-p)

\end{aligned}

\]

2.二项分布——离散型概率分布

概念:进行n次伯努利试验。(n>=1),当n=1,二项分布就是伯努利分布

n次试验中总共成功的次数为k的概率 \(P(X=k;n,p)=C_n^k*p^k*(1-p)^{n-k}\)

期望 $ E(X)=np $

期望的推导

\[

\begin{aligned}

E(X) &= \sum_{k=0}^{n}k*P(X=k)\&=\sum_{k=0}^{n}k*\frac{n!}{k!(n-k)!}p^k (1-p)^{n-k}\&=np\sum_{k=1}^{n}\frac{(n-1)!}{(k-1)!(n-k)!}p^{k-1} (1-p)^{(n-k)}\&=np

\end{aligned}

\]

方差$ D(X)=np(1-p) $

方差的推导

\[

\begin{aligned}

D(X) &= E(X^2)-E^2(X)\&=E[X(X-1)+X]-n^2p^2=E[X(X-1)]+np-n^2p^2

\end{aligned}

\]

\[

\begin{aligned}

E[X(X-1)] &= \sum_{k=0}^{n}k(k-1)*P(X=k)\&= \sum_{k=0}^{n}k(k-1)*\frac{n!}{k!(n-k)!}p^k(1-p)^{n-k}\&=n(n-1)p^2\sum_{k=2}^{n}\frac{(n-2)!}{(k-2)!(n-k)!}p^{k-2}(1-p)^{n-k}\&=n(n-1)p^2

\end{aligned}

\]

\[

\begin{aligned}

D(X)&=n(n-1)p^2+np-n^2p^2\&=np(1-p)

\end{aligned}

\]

3.泊松分布——离散型概率分布

泰勒展开式

\[

\begin{aligned}

e^x&=1+x+\frac{x^2}{2!}+\frac{x^3}{3!}+\cdots+ \frac{x^n}{n!}+R_n\1&=e^{-x}+xe^{-x}+\frac{x^2}{2!}e^{-x}+\frac{x^3}{3!}e^{-x}+\cdots+\frac{x^n}{n!}e^{-x}+R_ne^{-n}

\end{aligned}

\]

通项 $ \frac{x^k}{k!}e^{-x} $ ---> \(\frac{\lambda^k}{k!}e^{-\lambda}\)

概率分布\(P(X=k)=\frac{\lambda^k}{k!}e^{-\lambda},\lambda>0,k=0,1,2,\cdots\)

期望

\[

\begin{aligned}

E(X)&=\sum_{k=0}^{\infty}k*f(x)\&=\sum_{k=0}^{\infty}k*\frac{\lambda^k}{k!}e^{-\lambda}\&=\lambda\sum_{k=1}^{\infty}\frac{\lambda^{k-1}}{(k-1)!}e^{-\lambda}\&=\lambda

\end{aligned}

\]

方差

\[

\begin{aligned}

D(X) &= E(X^2)-E^2(X)\&=E[X(X-1)+X]-E^2(X)\&=E[X(X-1)]+E(X)-E^2(X)\&=E[X(X-1)+\lambda-\lambda^2

\end{aligned}

\]

\[

\begin{aligned}

E[X(X-1)&=\sum_{k=0}^{\infty}k(k-1)*\frac{\lambda^k}{k!}e^{-\lambda}\&=\lambda^2\sum_{k=2}^{\infty}\frac{\lambda^{k-2}}{(k-2)!}e^{-\lambda}\&=\lambda^2

\end{aligned}

\]

\[

\begin{aligned}

D(X)&=E[X(X-1)]+E(X)-E^2(X)=\lambda^2+\lambda-\lambda^2=\lambda

\end{aligned}

\]

泊松分布的期望和方差都是参数\(\lambda\)!

4.均匀分布——连续型概率分布

概率密度函数为

\[

f(x)=\left\{

\begin{aligned}

&\frac{1}{b-a},&a<x<b\&0,&others

\end{aligned}

\right.

\]

期望\(E(X)=\int_{-\infty}^{\infty}x*f(x)dx=\frac{a+b}{2}\)

方差\(D(X)=E(X^2)-E^2(X)=\int_{a}^{b}x^2*\frac{1}{b-a}dx-\frac{(a+b)^2}{4}=\frac{(b-a)^2}{12}\)

5.指数分布——连续型概率分布

概率密度函数为

\[

f(x)=\left\{

\begin{aligned}

&\frac{1}{\theta}e^{-\frac{x}{\theta}},&x>0,\&0,&x\leq0

\end{aligned}

\right.

\]

其中\(\theta>0\)

期望

\[

\begin{aligned}

E(X)&=\int_0^{+\infty}x*f(x)dx\&=\int_0^{\infty}x\frac{1}{\theta}e^{-\frac{x}{\theta}}dx\&=-\int_0^{\infty}xd(e^{-\frac{x}{\theta}})\&=-[xe^{-\frac{x}{\theta}}|_0^{\infty}-\int_0^{\infty}e^{-\frac{x}{\theta}}dx]\&=\theta

\end{aligned}

\]

方差

\[

\begin{aligned}

D(X)&=E(X^2)-E^2(X)\&=\int_0^{+\infty}x^2\frac{1}{\theta}e^{-\frac{x}{\theta}}-\theta^2\&=2\theta^2-\theta^2\&=\theta^2

\end{aligned}

\]

6.正态分布/高斯分布

设随机变量X服从正态分布,即X~\(N(\mu,\sigma^2)\)

概率密度函数为

\[

f(x)=\frac{1}{\sqrt{2\pi}\sigma}e^{-\frac{(x-\mu)^2}{2\sigma^2}}

\]

期望\(E(X)=\mu\)

方差\(D(X)=\sigma^2\)