标签:之间 rename database sde 添加 fill create symbols 6.4

本文翻译自《Demo Week: class(Monday) <- tidyquant》

原文链接:http://www.business-science.io/code-tools/2017/10/23/demo_week_tidyquant.html

tidyquant 的用途使用 tidyquant 的六大理由:

geom_ma)tidyquant 会自动加载 tidyverse 和各种金融、时间序列分析包,这使得它成为任何金融或时间序列分析的理想起点。该教程将会介绍前两个主题。其他主题请查看 tidyquant 的文档。

请先安装 tidyquant:

# Install libraries

install.packages("tidyquant")加载 tidyquant。

# Load libraries

library(tidyquant) # Loads tidyverse, financial pkgs, used to get and manipulate datatq_get:获得数据使用 tq_get() 获得网络数据。tidyquant 提供了大量 API 用于连接包括 Yahoo! Finance、FRED Economic Database、Quandl 等等在内的数据源。

将一列股票代码传入 tq_get(),同时设置 get = "stock.prices"。可以添加 from 和 to 参数设置数据的起始和结束日期。

# Get Stock Prices from Yahoo! Finance

# Create a vector of stock symbols

FANG_symbols <- c("FB", "AMZN", "NFLX", "GOOG")

# Pass symbols to tq_get to get daily prices

FANG_data_d <- FANG_symbols %>%

tq_get(

get = "stock.prices",

from = "2014-01-01", to = "2016-12-31")

# Show the result

FANG_data_d## # A tibble: 3,024 x 8

## symbol date open high low close volume adjusted

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 FB 2014-01-02 54.83 55.22 54.19 54.71 43195500 54.71

## 2 FB 2014-01-03 55.02 55.65 54.53 54.56 38246200 54.56

## 3 FB 2014-01-06 54.42 57.26 54.05 57.20 68852600 57.20

## 4 FB 2014-01-07 57.70 58.55 57.22 57.92 77207400 57.92

## 5 FB 2014-01-08 57.60 58.41 57.23 58.23 56682400 58.23

## 6 FB 2014-01-09 58.65 58.96 56.65 57.22 92253300 57.22

## 7 FB 2014-01-10 57.13 58.30 57.06 57.94 42449500 57.94

## 8 FB 2014-01-13 57.91 58.25 55.38 55.91 63010900 55.91

## 9 FB 2014-01-14 56.46 57.78 56.10 57.74 37503600 57.74

## 10 FB 2014-01-15 57.98 58.57 57.27 57.60 33663400 57.60

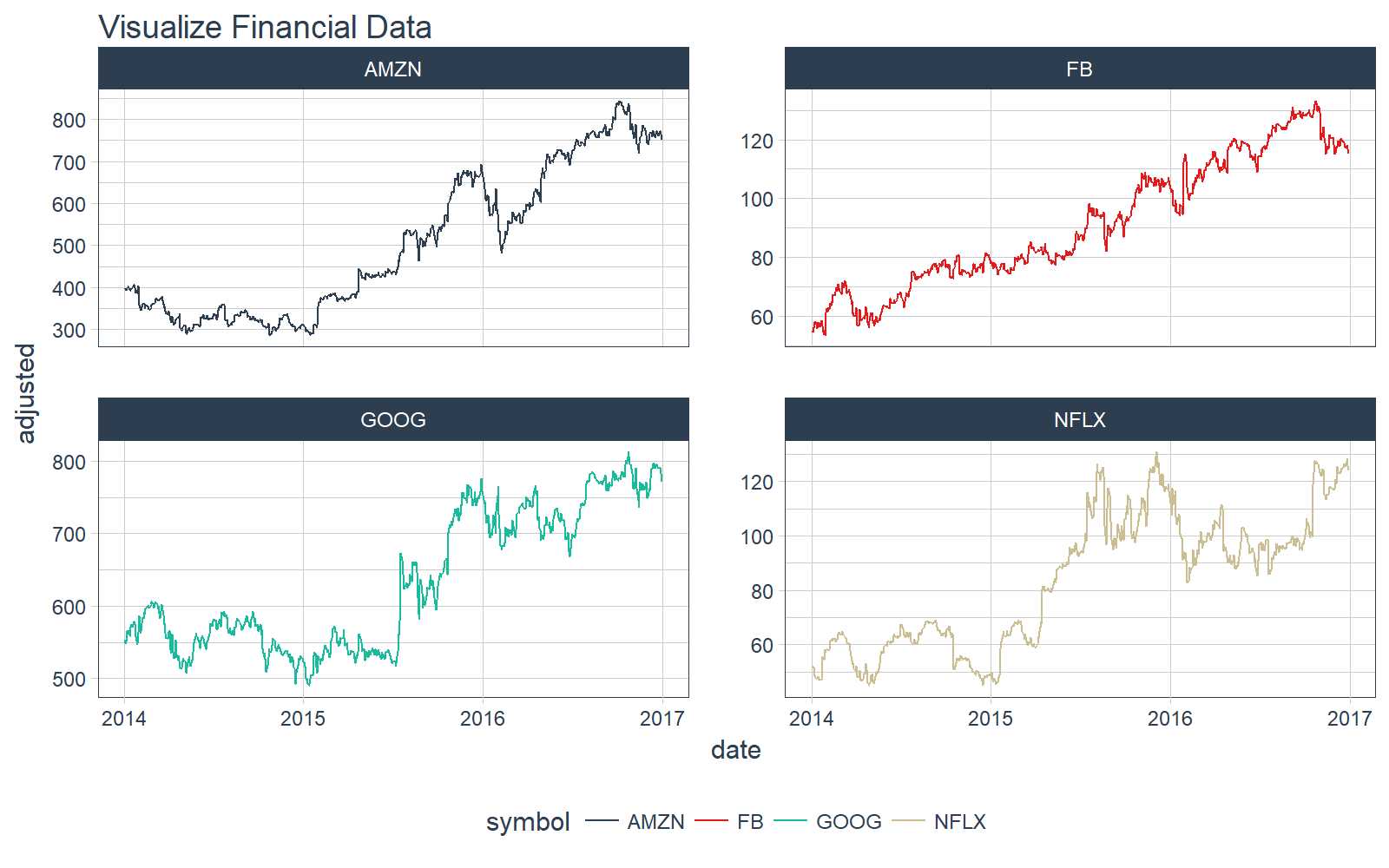

## # ... with 3,014 more rows可以使用 ggplot2 画出上述结果。使用 tidyquant 提供的主题(调用 theme_tq() 和 scale_color_tq())实现金融、商务风格的可视化效果。

# Plot data

FANG_data_d %>%

ggplot(aes(x = date, y = adjusted, color = symbol)) +

geom_line() +

facet_wrap(~ symbol, ncol = 2, scales = "free_y") +

theme_tq() +

scale_color_tq() +

labs(title = "Visualize Financial Data")

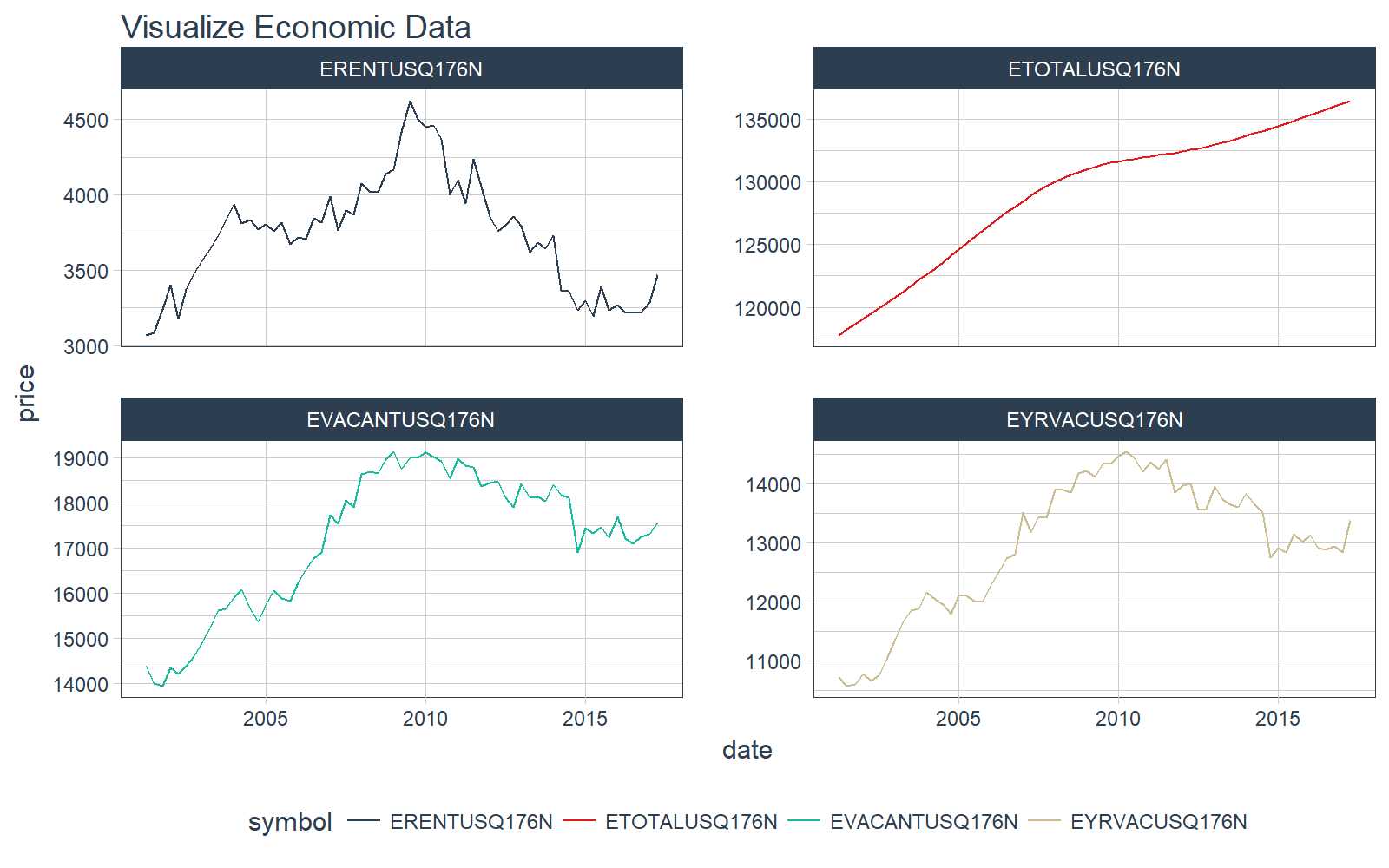

下面的例子来自房地美副首席经济学家 Leonard Kieffer 近期的文章——《A (TIDYQUANT)UM OF SOLACE》。我们将使用 tq_get() 并设置参数 get = "economic.data" 来从 FRED 经济数据库获取数据。

将一列 FRED 代码传递到 tq_get()。

# Economic Data from the FRED

# Create a vector of FRED symbols

FRED_symbols <- c(‘ETOTALUSQ176N‘, # All housing units

‘EVACANTUSQ176N‘, # Vacant

‘EYRVACUSQ176N‘, # Year-round vacant

‘ERENTUSQ176N‘) # Vacant for rent

# Pass symbols to tq_get to get economic data

FRED_data_m <- FRED_symbols %>%

tq_get(get="economic.data", from = "2001-04-01")

# Show results

FRED_data_m## # A tibble: 260 x 3

## symbol date price

## <chr> <date> <int>

## 1 ETOTALUSQ176N 2001-04-01 117786

## 2 ETOTALUSQ176N 2001-07-01 118216

## 3 ETOTALUSQ176N 2001-10-01 118635

## 4 ETOTALUSQ176N 2002-01-01 119061

## 5 ETOTALUSQ176N 2002-04-01 119483

## 6 ETOTALUSQ176N 2002-07-01 119909

## 7 ETOTALUSQ176N 2002-10-01 120350

## 8 ETOTALUSQ176N 2003-01-01 120792

## 9 ETOTALUSQ176N 2003-04-01 121233

## 10 ETOTALUSQ176N 2003-07-01 121682

## # ... with 250 more rows和金融数据一样,使用 ggplot2 画图,使用 tidyquant 提供的主题(调用 theme_tq() 和 scale_color_tq())实现金融、商务风格的可视化效果。

# Plot data

FRED_data_m %>%

ggplot(aes(x = date, y = price, color = symbol)) +

geom_line() +

facet_wrap(~ symbol, ncol = 2, scales = "free_y") +

theme_tq() +

scale_color_tq() +

labs(title = "Visualize Economic Data")

tq_transmute 和 tq_mutate 转换数据函数 tq_transmute() 和 tq_mutate() 可以使 xts、zoo 和 quantmod 中的函数调用更“tidy”。这里直接介绍使用,“可用函数”一节罗列了已经整合进 tidyquant 的若干其他函数。

tq_transmutetq_transmute() 与 tq_mutate() 之间的区别在于 tq_transmute() 将返回一个新的数据框对象,而 tq_mutate() 则在原有数据框的基础上横向添加数据(例如,增加一列)。当数据因为改变周期而改变行数时,tq_transmute() 特别有用。

tq_transmute下面的例子将改变数据的周期,从每日数据变为月度数据。这时,你需要使用 tq_transmute() 来完成这一操作,因为数据的行数改变了。

# Change periodicity from daily to monthly using to.period from xts

FANG_data_m <- FANG_data_d %>%

group_by(symbol) %>%

tq_transmute(

select = adjusted,

mutate_fun = to.period,

period = "months")

FANG_data_m## # A tibble: 144 x 3

## # Groups: symbol [4]

## symbol date adjusted

## <chr> <date> <dbl>

## 1 FB 2014-01-31 62.57

## 2 FB 2014-02-28 68.46

## 3 FB 2014-03-31 60.24

## 4 FB 2014-04-30 59.78

## 5 FB 2014-05-30 63.30

## 6 FB 2014-06-30 67.29

## 7 FB 2014-07-31 72.65

## 8 FB 2014-08-29 74.82

## 9 FB 2014-09-30 79.04

## 10 FB 2014-10-31 74.99

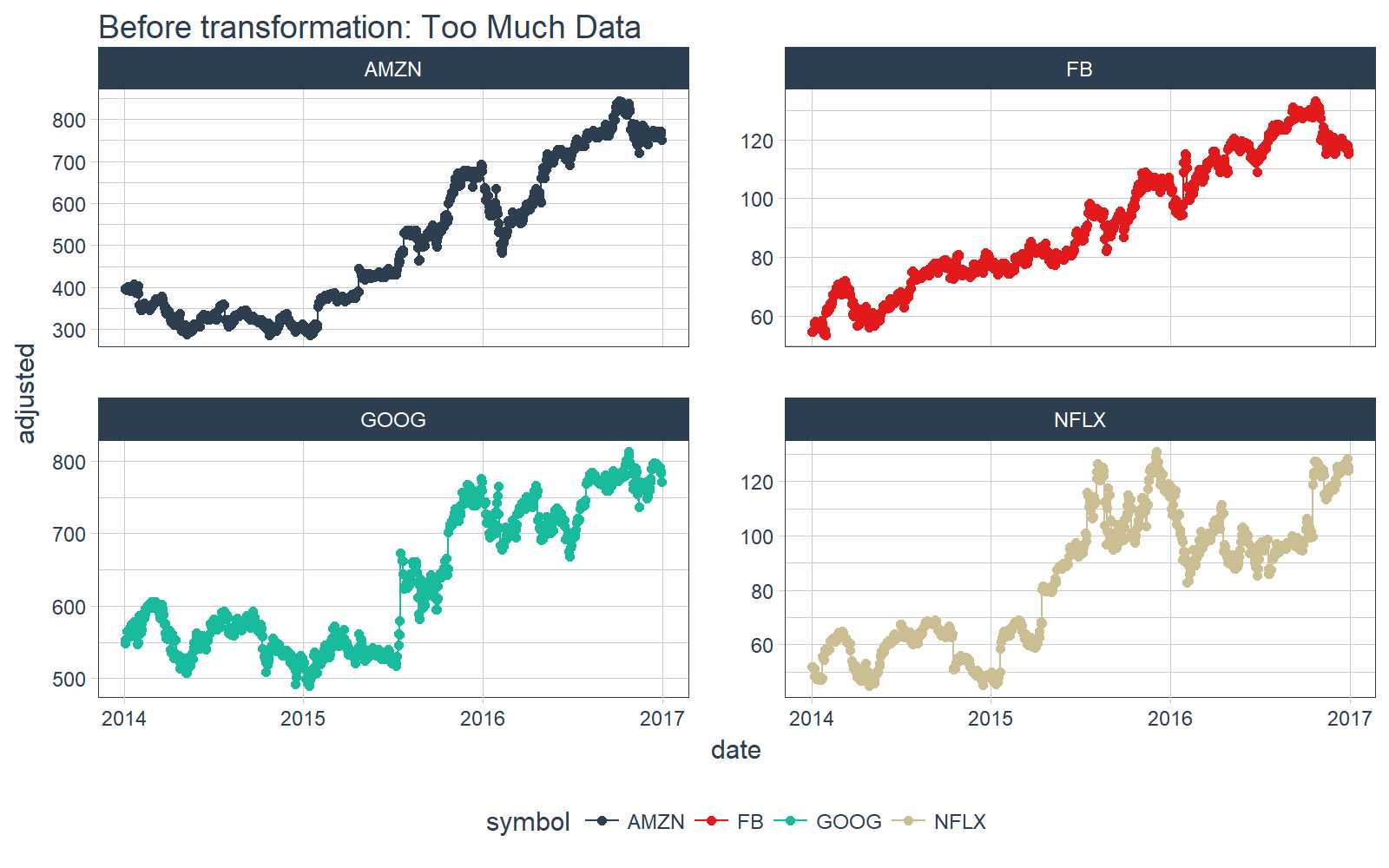

## # ... with 134 more rows改变数据周期可以缩减数据量。一些注意事项项:

theme_tq() 和 scale_color_tq() 用来绘制商务风格的图。tibbletime 包的教程,tibbletime 以另外一种标准处理基于时间的操作。# Daily data

FANG_data_d %>%

ggplot(aes(date, adjusted, color = symbol)) +

geom_point() +

geom_line() +

facet_wrap(~ symbol, ncol = 2, scales = "free_y") +

scale_color_tq() +

theme_tq() +

labs(title = "Before transformation: Too Much Data")

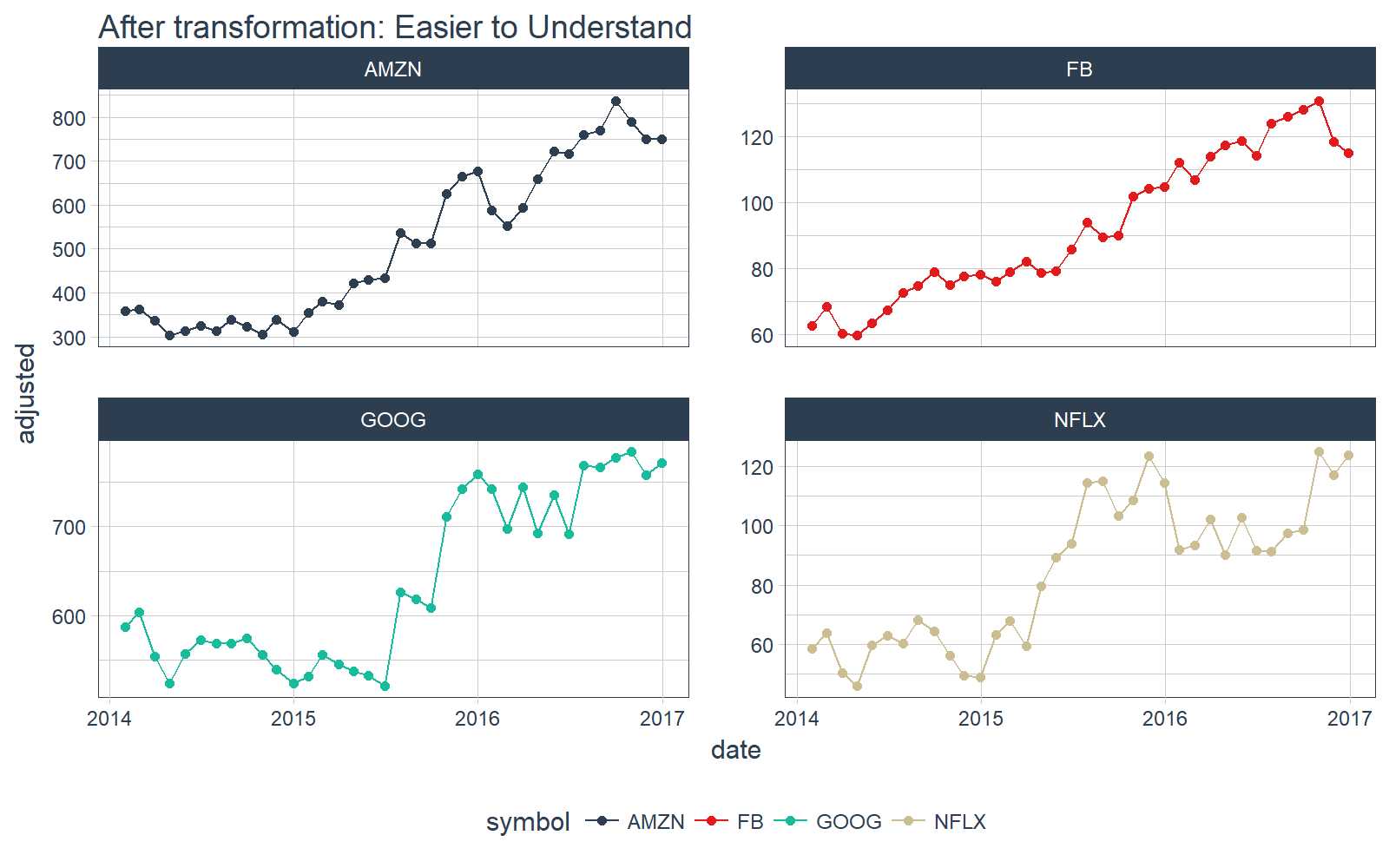

用 tq_transmute() 转变成月度数据后容易理解多了。

# Monthly data

FANG_data_m %>%

ggplot(aes(date, adjusted, color = symbol)) +

geom_point() +

geom_line() +

facet_wrap(~ symbol, ncol = 2, scales = "free_y") +

scale_color_tq() +

theme_tq() +

labs(title = "After transformation: Easier to Understand")

tq_mutatetq_mutate() 函数基于 xts 包为数据添加新的列。正因为这样,当返回数据不止一列时,tq_mutate() 显得特别有用(dplyr::mutate() 就没有这样的功能)。

tq_mutate 与滞后数据一个关于 lag.xts 的例子。通常我们需要不只一列滞后数据,这正是 tq_mutate() 擅长的。下面,为原数据添加五列滞后数据。

# Lags - Get first 5 lags

# Pro Tip: Make the new column names first, then add to the `col_rename` arg

column_names <- paste0("lag", 1:5)

# First five lags are output for each group of symbols

FANG_data_d %>%

select(symbol, date, adjusted) %>%

group_by(symbol) %>%

tq_mutate(

select = adjusted,

mutate_fun = lag.xts,

k = 1:5,

col_rename = column_names)## # A tibble: 3,024 x 8

## # Groups: symbol [4]

## symbol date adjusted lag1 lag2 lag3 lag4 lag5

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 FB 2014-01-02 54.71 NA NA NA NA NA

## 2 FB 2014-01-03 54.56 54.71 NA NA NA NA

## 3 FB 2014-01-06 57.20 54.56 54.71 NA NA NA

## 4 FB 2014-01-07 57.92 57.20 54.56 54.71 NA NA

## 5 FB 2014-01-08 58.23 57.92 57.20 54.56 54.71 NA

## 6 FB 2014-01-09 57.22 58.23 57.92 57.20 54.56 54.71

## 7 FB 2014-01-10 57.94 57.22 58.23 57.92 57.20 54.56

## 8 FB 2014-01-13 55.91 57.94 57.22 58.23 57.92 57.20

## 9 FB 2014-01-14 57.74 55.91 57.94 57.22 58.23 57.92

## 10 FB 2014-01-15 57.60 57.74 55.91 57.94 57.22 58.23

## # ... with 3,014 more rowstq_mutate 与滚动函数另一个例子,应用 xts 中的滚动函数 roll.apply()。让我们借助函数 quantile() 得到滚动分位数。下面是每个函数的参数:

tq_mutate 的参数:

select = adjusted,只选择复权修正过的数据列。该参数也可以不填,或选择其他不同的列。mutate_fun = rollapply,这是一个 xts 函数,将会以 “tidy” 的方式(分组)调用。rollapply 的参数:

width = 5,告诉 rollapply 计算窗口的周期(长度)是多少。by.column = FALSE,rollapply() 函数默认对每一列分别操作,然而我们要把所有列放在一起操作。FUN = quantile,quantile() 正是要被滚动调用的函数。quantile 的参数:

probs = c(0, 0.025, ...),计算这些概率的分位数。na.rm = TRUE,quantile 会去掉遇到的 NA 值。# Rolling quantile

FANG_data_d %>%

select(symbol, date, adjusted) %>%

group_by(symbol) %>%

tq_mutate(

select = adjusted,

mutate_fun = rollapply,

width = 5,

by.column = FALSE,

FUN = quantile,

probs = c(0, 0.025, 0.25, 0.5, 0.75, 0.975, 1),

na.rm = TRUE)## # A tibble: 3,024 x 10

## # Groups: symbol [4]

## symbol date adjusted X0. X2.5. X25. X50. X75. X97.5.

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 FB 2014-01-02 54.71 NA NA NA NA NA NA

## 2 FB 2014-01-03 54.56 NA NA NA NA NA NA

## 3 FB 2014-01-06 57.20 NA NA NA NA NA NA

## 4 FB 2014-01-07 57.92 NA NA NA NA NA NA

## 5 FB 2014-01-08 58.23 54.56 54.575 54.71 57.20 57.92 58.199

## 6 FB 2014-01-09 57.22 54.56 54.824 57.20 57.22 57.92 58.199

## 7 FB 2014-01-10 57.94 57.20 57.202 57.22 57.92 57.94 58.201

## 8 FB 2014-01-13 55.91 55.91 56.041 57.22 57.92 57.94 58.201

## 9 FB 2014-01-14 57.74 55.91 56.041 57.22 57.74 57.94 58.201

## 10 FB 2014-01-15 57.60 55.91 56.041 57.22 57.60 57.74 57.920

## # ... with 3,014 more rows, and 1 more variables: X100. <dbl>已经介绍了如何将 xts 函数和 tq_transmute 与 tq_mutate 联合使用。还有许多 xts 函数可以以 “tidy” 的方式使用!用 tq_transmute_fun_options() 查看其他可用函数。

# Available functions

# mutate_fun =

tq_transmute_fun_options()## $zoo

## [1] "rollapply" "rollapplyr" "rollmax"

## [4] "rollmax.default" "rollmaxr" "rollmean"

## [7] "rollmean.default" "rollmeanr" "rollmedian"

## [10] "rollmedian.default" "rollmedianr" "rollsum"

## [13] "rollsum.default" "rollsumr"

##

## $xts

## [1] "apply.daily" "apply.monthly" "apply.quarterly"

## [4] "apply.weekly" "apply.yearly" "diff.xts"

## [7] "lag.xts" "period.apply" "period.max"

## [10] "period.min" "period.prod" "period.sum"

## [13] "periodicity" "to.daily" "to.hourly"

## [16] "to.minutes" "to.minutes10" "to.minutes15"

## [19] "to.minutes3" "to.minutes30" "to.minutes5"

## [22] "to.monthly" "to.period" "to.quarterly"

## [25] "to.weekly" "to.yearly" "to_period"

##

## $quantmod

## [1] "allReturns" "annualReturn" "ClCl"

## [4] "dailyReturn" "Delt" "HiCl"

## [7] "Lag" "LoCl" "LoHi"

## [10] "monthlyReturn" "Next" "OpCl"

## [13] "OpHi" "OpLo" "OpOp"

## [16] "periodReturn" "quarterlyReturn" "seriesAccel"

## [19] "seriesDecel" "seriesDecr" "seriesHi"

## [22] "seriesIncr" "seriesLo" "weeklyReturn"

## [25] "yearlyReturn"

##

## $TTR

## [1] "adjRatios" "ADX" "ALMA"

## [4] "aroon" "ATR" "BBands"

## [7] "CCI" "chaikinAD" "chaikinVolatility"

## [10] "CLV" "CMF" "CMO"

## [13] "DEMA" "DonchianChannel" "DPO"

## [16] "DVI" "EMA" "EMV"

## [19] "EVWMA" "GMMA" "growth"

## [22] "HMA" "KST" "lags"

## [25] "MACD" "MFI" "momentum"

## [28] "OBV" "PBands" "ROC"

## [31] "rollSFM" "RSI" "runCor"

## [34] "runCov" "runMAD" "runMax"

## [37] "runMean" "runMedian" "runMin"

## [40] "runPercentRank" "runSD" "runSum"

## [43] "runVar" "SAR" "SMA"

## [46] "SMI" "SNR" "stoch"

## [49] "TDI" "TRIX" "ultimateOscillator"

## [52] "VHF" "VMA" "volatility"

## [55] "VWAP" "VWMA" "wilderSum"

## [58] "williamsAD" "WMA" "WPR"

## [61] "ZigZag" "ZLEMA"

##

## $PerformanceAnalytics

## [1] "Return.annualized" "Return.annualized.excess"

## [3] "Return.clean" "Return.cumulative"

## [5] "Return.excess" "Return.Geltner"

## [7] "zerofill"标签:之间 rename database sde 添加 fill create symbols 6.4

原文地址:https://www.cnblogs.com/xuruilong100/p/9217515.html